MEMBERSHIP LOGIN

MEMBERSHIP LOGIN JOIN PRI

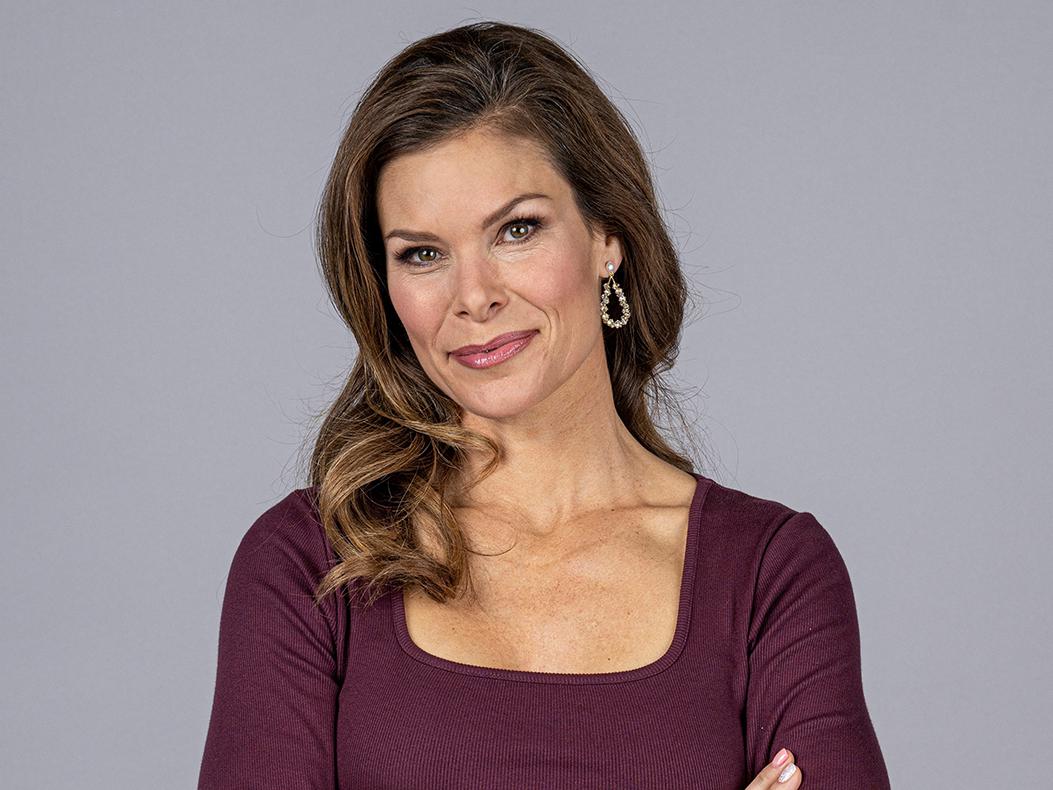

JOIN PRIMember Check-In: John Johnson

PRI Membership encompasses a wide range of companies including the Spartan Group, which focuses on management services to middle-market business owners in the performance segment.

There is a wave of foreseeable changes coming in the aftermarket and racing-component industries, unfolding as longstanding entrepreneurs retire and the growth of electrification presents both challenges and opportunities for business owners and investors. Navigating these financial and organizational pathways is the specialty of John O. Johnson, co-founder of the Spartan Group in Pasadena, California, which provides advisory and management services to business owners in what the investment world calls the middle market.

What’s that? In business parlance, the middle market is made up of companies, generally privately owned or closely held, with revenues running from $5 million to $1 billion annually. They account for about a third of the US private-sector GDP and employ about a quarter of the nation’s workforce. They’re also very well represented in the automotive aftermarket and performance sectors, which account for a substantial chunk of the Spartan Group’s clients. Essentially, middle-market businesses are too big to be called family owned and too small to qualify as multinationals.

Before co-founding the Spartan Group with his partners, Johnson managed an IPO for Edelbrock and went on to form financial management relationships with K&N Filters, Dart Machinery, Aeromotive and Jesel, among others. By the early 2000s, Johnson was focusing on performance industries as clients for his investment-banking services. He worked in mergers and acquisitions on both the buy and sell sides, helped business owners secure investment capital, and counseled them on taking their firms public. He co-founded the Spartan Group in 2003, and more recently was named SEMA’s Person of the Year in 2017 for contemporizing the association’s organizational and financial discipline.

“A more apt description than middle market is family owned or entrepreneurially owned companies,” Johnson explained. “We’re an investment bank focused on them. Most of my clients are not private equity-owned companies. We sell some of them to private equity, and we buy some companies from private equity, but my clients are long-term relationships. Sometimes it’s called a boutique bank because of the client quality. Private equity companies tend to be more institutionally owned, backed by limited partners that are often pension funds, insurance companies or governmental entities. That’s typically not our client base.

“We get to know companies for multiple years, often decades, and work with them before there’s a real transaction,” he continued. “We’re talking with them about the industry, about technology, about the RPM Act, about emissions standards, about electric vehicle conversions, even mundane things like sales and use tax compliance and personal-data compliance, any kind of advice that involves business in the performance aftermarket. Effectively, we’re problem solvers, but we also bring transactional and financial advice.”

The Spartan Group’s client base ranges from OE aftermarket suppliers and full-system manufacturers to powersports and Class 8 truck builders. Johnson estimated, however, that performance is 75% of his business, with five to 15 major transactions per year.

The industry’s potential challenges in the near-term fall into two broad categories starting with demographics, as the baby boomer generation of business owners ages out. “The generational shift is from the boomers to what’s now the largest consumer segment in our society, which is millennials,” Johnson said. “Buyer appetite is toward millennials, so the boomers are transitioning either to the next generation of family ownership, or in more cases than not, to new owners. That’s an overarching issue.”

Johnson foresees the industry’s current crunch of supply and labor shortages easing within six to 12 months. A parallel issue, from an immediacy standpoint, is his view that e-commerce and direct-to-buyer engagement are industry priorities. “There’s a huge movement toward buying direct from the manufacturer,” he said. “That can increase its margin, and the manufacturer can talk directly to the consumer. On the EV side, Tesla does it. It’s like Walmart versus Amazon.”

The other key consideration for Spartan is the intertwining of technological and regulatory realties, he added. “The most important ones are adherence to the Clean Air Act of 1986, the most pivotal issue in the industry today, which is why the RPM Act that SEMA and PRI support is so important. Consumers have to have the right to choose to convert an OE vehicle and use it on the race track. We advise a lot of our companies on strategies for dealing with that.

“The related challenge is how the industry adapts to electric-vehicle conversion,” Johnson said. “We have a view at this firm that EV conversion is going to be healthy over time. There is a base of more than 290 million installed ICE vehicles in North America. Roughly 4% of vehicles sold this year are going to be full EV—not hybrid. And even though the infrastructure bill will have a lot of stimulus to transition to them, our studies show that 19% of new-car sales in 2030 are going to be EV. That means 81% are still going to be ICE. And that’s on top of the 280 or 290 million that are still in the marketplace. With the stimulus, maybe that goes to 25% instead of 19. The point is, ICE engines are going be around for a while, and the EVs are going to have a healthy market share, growing at over 21% over the next decade, even without the big juice or stimulus. So we’re going to have to coexist, and that coexistence is really the industry’s other major challenge.”

Major EV suppliers will likely experience their own consolidations before exploring future mergers with the aftermarket, Johnson predicted. What likely won’t change is that buyer enthusiasm, namely the car person or racer, will continue to power the aftermarket during the EV pivot. “We’ve seen dramatic growth in the pandemic as people have stayed home and wrenched on their vehicles, invested stimulus money in their projects. They’re enthusiasts. It’s a way of life. It’s a lifestyle, not a hobby, and that’s still the driver in the market. We’re a car culture. Really, the discussion still begins and ends there. That’s what makes this such a fun industry.”